Do I really need Travel Insurance?

- Dorina

- Nov 26, 2018

- 7 min read

As a Travel Professional, a question that comes up a lot is “Do I really need Travel Insurance?”

The short answer is yes, always. The long answer?

Life is always one of those unpredictable things. Sometimes our best laid plans don’t go according to plan. And finding yourself facing a bill that’s hundreds or thousands of dollars is a really difficult situation to be in for anyone. So make sure you’re protected.

What is Travel Insurance?

Travel Insurance is a short term insurance plan that protects you, your family and your trip. It can help cover an array of costs incurred from a minor inconvenience to the downright tragic. It can be purchased for domestic as well as international travel.

What are the different “legs” of Travel Insurance?

Travel Insurance is a bit like a chair, and is comprised of four different legs - Trip Interruption and Cancellation, Medical, Accidental Death and Dismemberment and Baggage. Travelers can mix and match or get all four as a package, though bundling all four is often the most cost effective route.

How much does Insurance cost?

The cost of Travel Insurance can vary dramatically between providers and is typically based on the cost of your non-refundable costs (things like airline tickets or hotels, but not your budget for eating out when in destination or your planned, but unbooked, excursions).

Generally, the cost difference has to do with what you are and are not covered for, as well as the coverage amounts. Costs can also be impacted by age and underlying medical conditions. Usually the higher the price, the better the coverage. If you’re trying to plan out a trip I recommend preparing for full coverage insurance to be about 5-10% of the total trip cost. That way when your Travel Professional (hey, that’s me!) is researching your trip for you, you won’t be surprised by insurance as an unplanned cost that might take you over what you were planning on spending.

So...what do the different "legs" cover?

Each component does something different.

Trip Cancellation - if you have to cancel your trip before you go, this will refund some or all of the costs, depending on your coverage.

Trip Interruption - similar to Cancellation, but this is in effect once you’ve departed for your trip. So this covers you if you have to interrupt a trip already in progress.

These two are not always packaged together, so that’s important to be aware of when looking at different policies.

Medical - this helps cover you for unexpected medical situations when traveling, like doctors, hospital stays or medication.

Accidental Death and Dismemberment - it’s unfortunate, but sometimes people die while on a trip, or they may lose a body part. This pays out to you or your beneficiary an amount if either should happen.

Baggage - a recent study found that only 1% of bags are lost and only about 3% are mishandled. Still, when you arrive to your destination and your bag does not, things can get stressful. This coverage pays for or reimburses you for expenses, like purchasing new clothes.

What are some real life examples?

There are a ton, and a quick search on Go Fund Me will pull up a whole host of people who didn’t get Travel Insurance asking the public for money to help them cover medical expenses or other very stressful costs, like returning a body to the country of residence.

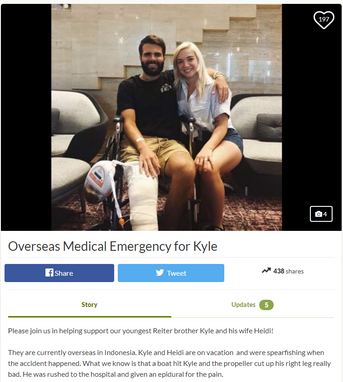

But let’s say you’re off on vacation and you feel ill part way through. As Canadians, with universal health care, we often don’t realize just how expensive medical care can be, especially in certain countries like the USA. But let’s say it starts with a visit to the doctor and they determine that you need a hospital because you’ve contracted an illness. You’re admitted and provided medications. Let’s say it’s not serious, no surgery needed, but your stay in the hospital extends beyond your current flight time home. And your partner isn’t going home without you, and you have two children in tow under the age of 10, so now they have to stay longer too. So you have medical bills to pay, you have to extend your trip, change your flights (or get entirely new flights) and your family needs a hotel to stay. The expenses can add up quickly. Travel Insurance protects you.

There have also been reports of bed shortages in certain areas in Canada, which means if you’re in a safe location with a hospital bed overseas, your home province might not accept you back right away because they don’t have a bed for you, meaning your overseas hospital costs accumulate.

Another example - you’re off - bags are packed and you’re on the way down the highway to the airport. Along the way, there’s an accident and you’re stuck in traffic and miss your flight. Travel Insurance protects you.

Are all Insurances the same?

Short answer no.

It’s super important that you understand the policy being offered. Not all policies are of the same quality. Some policies will pay up front for you, others require you to keep your receipts and they reimburse you. And can you imagine facing a $50,000 hospital bill that you have to pay up front and get reimbursed for later?

In addition to what's in a policy, there are also different kinds of insurance.

- Single Trip Coverage

- Annual Coverage

- Family Coverage

- Student Coverage

- Business Coverage

And of course, all of the kinds can fluctuate as one ages. Often for folks who are seniors, travel insurance can be a bit of a tricky thing to navigate.

If I have insurance covered through work or my credit card, isn’t that enough?

Maybe.

But coverage and amounts are often quite limited through employer or credit card plans. So it’s really important to look through your coverage. If you think you need more, you can purchase more to supplement what you already have, or if an element is missing (say they cover Medical, but not Interruption and Cancellation and that’s super important to you), you can purchase that component to beef up pre-existing coverage.

And I can’t stress understanding your policy enough. A friend of mine traveled down to Mexico for surgery. The wait list in Canada was incredibly long - she could get the surgery in Mexico before anyone here had even called her for a consultation. Her coverage through work ended up being nullified because she was going for a medical procedure. On the way home (at a layover between flights) she collapsed and died. When they did the autopsy they found she had a pre-existing blood clot no one knew about and that was the cause of death. Her travel insurance was through work’s benefit plan and when her mom went to go and file a claim, they told her my friend wasn’t covered, even though the clot was entirely unrelated to the surgery.

Above is a screenshot of an unnamed Credit Card company's included Trip Interruption Insurance on one of their annual fee cards. But what if your flight home is over $1500? What if your flight is under $1499, but you also had to take a taxi to get to the airport? What if it required an unexpected hotel stay? This only seems to cover transportation and not accommodation. What if you're a family of 5 covered and flights total $7,500? And then what if the scenario isn't one of the covered reasons. Understanding a policy helps you weigh out the risks and the benefits much better.

Know your policy.

When should I buy insurance?

Honestly you can buy any time. I know with what my agency offers, there is a benefit to buying it within the first 3 days of booking. But I’ve also personally pulled the procrastinator card and booked insurance a month before departure.

The thing is, you’re only covered if you purchase, and upsets can happen at any time. Whether you purchase in the first 3 days of booking or whether you purchase a month from your trip, the cost is the same. So I recommend buying insurance when you buy your trip. The amount you pay goes further (because you’re protected longer) AND if something comes up unexpectedly, you have that insurance in place to deal with things, and it didn't cost you any extra.

If you book online and not through an agent I do have a word of warning - many sites offer insurance during the booking process. You do not have to agree to insurance at the time of booking to purchase it. So be careful before clicking yes, because the coverage might not be what you need it to be.

Above is a screen shot from Ryanair and a random flight I looked into for this blog article from London to Katowice (who doesn't love Poland in November?). The flight costs come to $171 and the insurance costs 8-12% of the trip cost. You'll notice that only cancellation is offered, but not trip interruption. The above is only available to citizens of the UK, but it does show how understanding what you are and are not getting can be tricky and sometimes a little hidden.

The Bottom Line

I have been an advocate for Travel Insurance since long before I became a Travel Professional. If a couple hundred dollars could save me from paying THOUSANDS later, it’s worth it. I’m lucky enough that I’ve never had to use my insurance, but that’s never stopped me from purchasing it for myself. Plus I want to know if anything happens to me, my family doesn’t have to stress about money to cover my bills.

And I just can’t stress enough to understand your coverage. I often suggest to my clients to get three quotes to be able to compare pricing and coverage. While some Trip Interruption will cover you as soon as you leave your door, others don’t cover you until you’ve completed the first leg of your trip. So if you have a connecting flight in Toronto you miss because of that accident on the way to the airport I mentioned above, one insurance will cover you for missing your flight out of Edmonton and the other won’t.

Still have questions?

Travel Insurance is sometimes a quirky thing; it can be hard to compare policies because you’re usually not dealing with an apples vs. apples situation and there are so many types and then there are even types within a type (basic, premium, deluxe etc.). So if you still have questions, feel free to connect with us and we can help you find the answers you’re looking for.

If you live in Alberta, we can also serve as a source for your travel insurance needs, so feel free to send me a message (there’s a contact form at the bottom of your page or shoot me an email at dorina.brown@dorinabrowntravel.com) and I’ll get you connected to our Insurance Department for a quote. What we offer does tend to be some of the best coverage in the province, so I do recommend considering us as one of your quotes.

Comments